- Analytics

- Market Sentiment

Dollar bullish bets rise on rate hike expectations

Bullish bets on US dollar rose to $14.7 billion from $10.2 billion against the major currencies during the previous week, according to the report of the Commodity Futures Trading Commission (CFTC) covering data up to October 11. Investor sentiment toward the dollar benefited from somewhat mixed economic data of the past week.

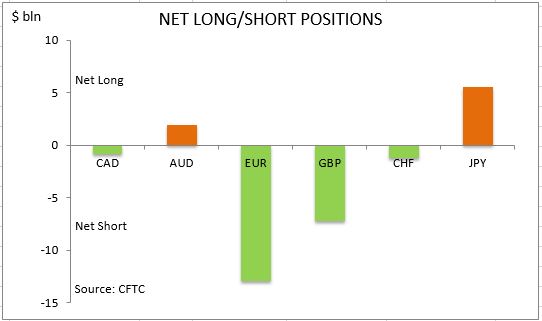

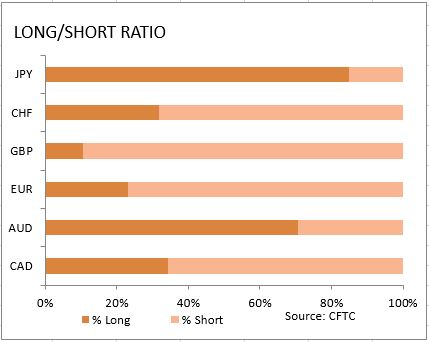

The Institute for Supply Management’s Services Index jumped to 57.1 in September from 51.4 in August, providing support to expectations for a rate hike before the end of the year. A reading of more than 50 indicates growth in activity. The jump in ISM Services PMI indicated the services sector expanded at the fastest pace in 11 months. Markit’s Services PMI also rose in September to 52.3 from 51 in August. But the growth in Factory Orders in August slowed to 0.2% over month from downwardly revised 1.4% in July, confirming declining business investment trend. Still it was better than expected. The labor market data were also less favorable: the Automatic Data Processing Inc. reported that private sector employers added 154000 jobs last month, down from 175000 in August. And official jobs report confirmed that nonfarm jobs grew 156 thousand in September, down from upwardly revised 167 thousand in August. Federal Reserve signaled at September meeting it plans one rate hike this year if US economic data are good. The data were good enough signaling the labor market strength endures, which supports the case for a Fed rate hike by the end of the year. Investors boosted dollar bullish bets on positive economic data. As is evident from the Sentiment table, sentiment deteriorated for euro, Japanese yen and Swiss franc. And the Australian dollar and Japanese yen remain the only two major currencies held net long against the US dollar.

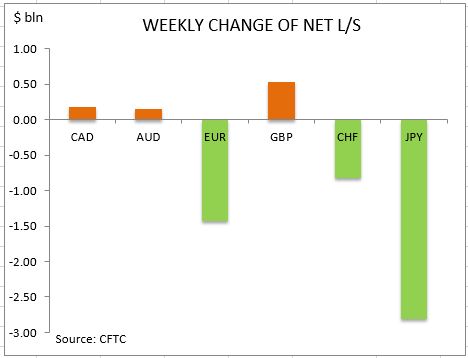

Investors’ view of the euro turned considerably more bearish after the European Central Bank stated rates will remain low until inflation gets up to the ECB's target and the central bank's decision-making body has not discussed reducing the pace of its monthly bond buying in response to reports ECB considered scaling back monthly bond purchases . The net short euro position widened by $1.4bn to $12.9bn. Investors increased both the gross longs and shorts by 8650 and 20063 contracts respectively. The British Pound sentiment improved despite news Prime Minister Theresa May plans to start exit negotiations no later than in March 2017. Many had expected the negotiations to start much later. Pound net shorts fell by $0.5 billion to $7.2 billion. The net short position in British Pound narrowed as investors cut both the gross longs and shorts by 6367 and 8469 contracts respectively. The bullish Japanese yen sentiment moderated significantly with the net long position in Japanese yen falling by $2.8bn to $5.5bn. Investors reduced the gross longs and increased shorts by 22707 and 79 contracts respectively.

The Canadian dollar sentiment improved marginally with the net shorts narrowing by $184 million to $0.8bn against the dollar. Investors cut both the gross longs and shorts. The bullish sentiment improved for the Australian dollar with net longs rising by $0.1bn to $1.9bn. Investors cut both the gross longs and gross shorts. The sentiment deteriorated considerably for the Swiss franc with the net shorts widening by $0.8bn to $1.1bn. Investors built both the gross longs and shorts.

CFTC Sentiment vs Exchange Rate

| October 11 2016 | Bias | Ex RateTrend | Position $ mln | Weekly Change |

| CAD | bearish | negative | -883 | 184 |

| AUD | bullish | negative | 1966 | 144 |

| EUR | bearish | negative | -12917 | -1428 |

| GBP | bearish | negative | -7228 | 532 |

| CHF | bullish | negative | -375 | 391 |

| JPY | bullish | negative | 8346 | -230 |

| Total | -10715 |

New Exclusive Analytical Tool

Any date range - from 1 day to 1 year

Any Trading Group - Forex, Stocks, Indices, etc.

Note:

This overview has an informative and tutorial character and is published for free. All the data, included in the overview, are received from public sources, recognized as more or less reliable. Moreover, there is no guarantee that the indicated information is full and precise. Overviews are not updated. The whole information in each overview, including opinion, indicators, charts and anything else, is provided only for familiarization purposes and is not financial advice or а recommendation. The whole text and its any part, as well as the charts cannot be considered as an offer to make a deal with any asset. IFC Markets and its employees under any circumstances are not liable for any action taken by someone else during or after reading the overview.

- Get Certificate

Last Sentiments

- 18Mar2021Weekly Top Gainers/Losers: Canadian dollar and Japanese yen

Over the past 7 days, prices for oil, non-ferrous metals and other mineral raw materials decreased but still remained high. As a result, the currencies...

- 10Mar2021Weekly Top Gainers/Losers: Canadian dollar and New Zealand dollar

Оil quotes continued to rise over the past 7 days. Against this background, the currencies of oil-producing countries, such as the Russian ruble and the...

- 4Mar2021Weekly Top Gainers/Losers: American dollar and South African rand

Over the past 7 days, oil quotes continued to grow. Precious metals, including gold, fell in price. Against this background, the shares of oil companies...