- Analytics

- Market Overview

Today we expect speech by the Fed Chairman, Janet Yellen - 2.7.2014

July began with the rapid growth in the world's stock markets. Two U.S. manufacturing indexes for June such as the final Manufacturing PMI from Markit and ISM Manufacturing were worse than expected. Nevertheless, large investors have decided that their values still show the normal dynamics of the U.S. economy and began actively buying shares.

The PMI rose to the highest level since May 2010 and amounted to 57.3 points. Construction costs rose in June by 0.1%. The trading volume on the U.S. exchanges was at its monthly average showing 5.8 billion shares yesterday. The Dow and S&P 500 refreshed their historical highs. They have been growing more than two years without any significant correction of at least 10%. The P/E coefficient for the S& P\500 reached its 4-year maximum. Meanwhile, American economists have lowered the forecasts for aggregate profit and revenue growth of companies from the S&P500 list to 5.2% and 3.2%, respectively. In early April they expect them to be increased increase by 7.3% and 3.7%. The reporting season for the second quarter of 2014 kicks out next week. Recall that on Friday, the U.S. markets are closed due to the holiday (Independence Day). Today, we will see the U.S. labor market data from ADP for June in the U.S. at 12-15 CET. It is is expected to be positive. We will also see the data on factory orders for May at 14-00 CET. The forecast is negative. Market participants believe that the ADP report is more important now and U.S. futures indexes are "in the black”. Jannet Yellen’s speech is expected at 15-00 CET.

European stocks rose yesterday after the U.S. stock market. The Economic data in the EU were slightly positive. The PMI manufacturing growth in the UK and France exceeded the forecasts. It fell slightly in Germany and Italy, but remained above 50 points, which is considered as the industry growth (when the PMI is lower than 50 points - fall). Today, the EU will show the PPI for May. The forecast is neutral.

The Nikkei has grown in line with the global trend. Tomorrow morning at 1-35 CET, we will see the Japanese PMI Composite and the service PMI, as well as the Ministry of Finance report on investment this week. In our opinion, the prognosis is slightly negative. Now Japanese stocks are corrected downwards.

The Oil price fell to the 3-week low on the fact that the war in Iraq does not influence the exports. Meanwhile today, at 14-30 CET we will see the data on its reserves in the United States. It is expected to decrease by 2.4 million barrels and the gasoline stocks to rise by 550 thousand barrels. The Projected National Hurricane Center predicts that the tropical storm "Arthur" in Miami may increase before the hurricane within two days. In this case, it is able to prevent the Oil import in the U.S. and further reduction in its reserves.

Gold continues to rise in spite of the U.S. stock market growth. Typically, they move in counterphase. Perhaps investors buy the precious metal for dollars becoming cheaper within three weeks. Assets of the world's largest gold fund (SPDR Gold Trust) increased within two consecutive days. Their cumulative growth was the highest since November 2011. We also note the Silver price growth.

The Copper prices increased due to good industrial PMI’s from China, the U.S., Europe and Japan. An additional positive today was the statement of the Ministry of Energy and Mineral Resources of Indonesia, the trial with the U.S. company Newmont Mining may take a long time. Recall that Indonesia has suspended the Copper exports from the beginning of the year on the backdrop of the struggle for increasing fees for U.S. companies, such as Newmont and Freeport-McMoRan, which own the main deposits of this metal in the country.

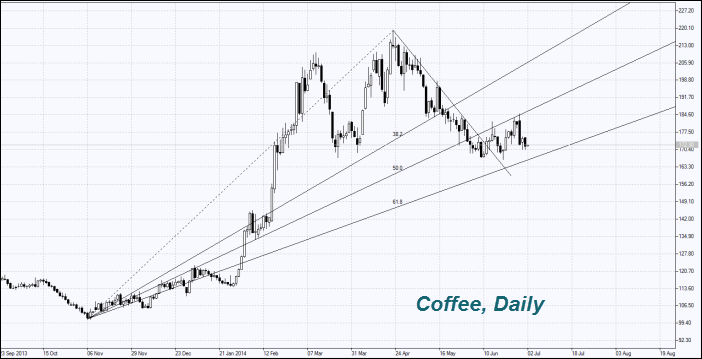

The Coffee prices fell after the announcement of the International Coffee Organization about reducing its global exports in May by 5.6% compared to May 2013 year. The coffee exports fell by 3.9% to 72.8 million bags within 8 months of the season 2013/2014.

- Get Certificate

See Also