- Analytics

- Market Overview

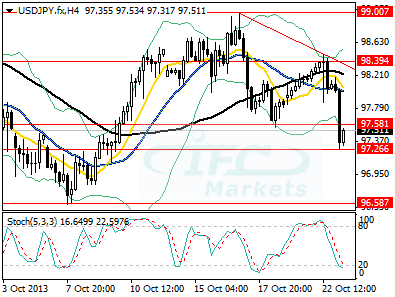

USD Dips to New 8-Month Low, Risk-off as Chinese Banks Cancel Debt - 23.10.2013

US employment report showed that September Non-Farm Payrolls were surprisingly at 148K, way below expectations of 182K while the August NFP was revised upward from 169K to 193K. Unemployment rate dropped slightly from 7.3% in August to 7.2% in September, while since June the rate dropped by 0.4%

USDJPY

- Get Certificate

See Also

Follow the Market with Our Live Tools and Calendars

Market Analysis Lab from Our Top Experts