- Analytics

- Market Overview

Investors ignored the good macroeconomic indicators from the U.S. during the whole last week - 28.4.2014

On Friday, the U.S. Dollar Index (USDIDX) proceeded in a neutral trend for the eighth consecutive day. All the last week, investors ignored the good U.S. macroeconomic indicators. On Friday, the increase in the consumer confidence index from the University of Michigan for April in the second reading significantly exceeded the forecasts and totaled 84.1 points. However, it has not caused the USD strengthening. Today at 15:00 CET, we will see the data on pending real estate transactions for March. We believe that the preliminary forecasts are positive for the U.S. Dollar.

The Japanese Yen strengthened slightly due to good retail sales data for March. It looks like depreciation on the USDJPY chart. Another piece of reporting will be released on Wednesday. At the same time, there will be the BOJ meeting held where the measures for further economy stimulation (emission increase) will be announced.

The British Pound (GBPUSD) slightly strengthened by the beginning of the period of annual dividend payments. Distributions to the shareholders were announced by 9 of the 20 largest British companies. It is assumed that they sold a part of their revenues in Dollars and Euros and bought the GBP’s. The total amount of dividends will be 30.7 billion Pounds. Tomorrow morning at 9:30 CET, there will be the Q1 UK GDP released. The preliminary forecast is positive.

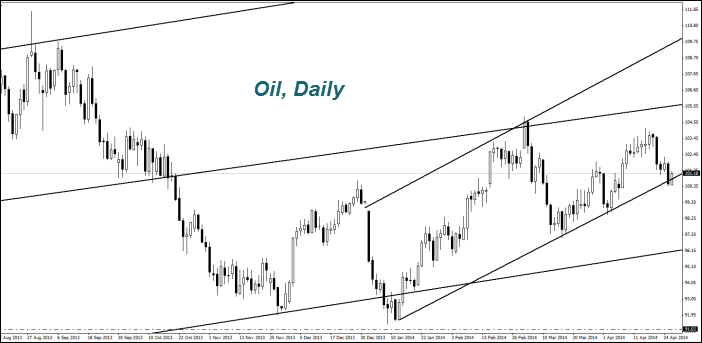

The (Oil, Brent) prices rose due to the possible entry of additional sanctions against Russia (7th country in the world by oil reserves). We do not exclude further Oil and Gas (Natgas) appreciation. The Natural gas reserves in the U.S. fell to the lowest level of 11 years.

As we predicted in previous reviews, the Coffee prices corrected downwards. Earlier, its quotes have grown substantially due to lower crop forecast in Brazil because of the drought. Now the price movements are affected by the weather forecasts in this country. As in the case of the rain, the coffee harvest may be higher than the current market expectations. Brazil is the third Coffee producer in the world.

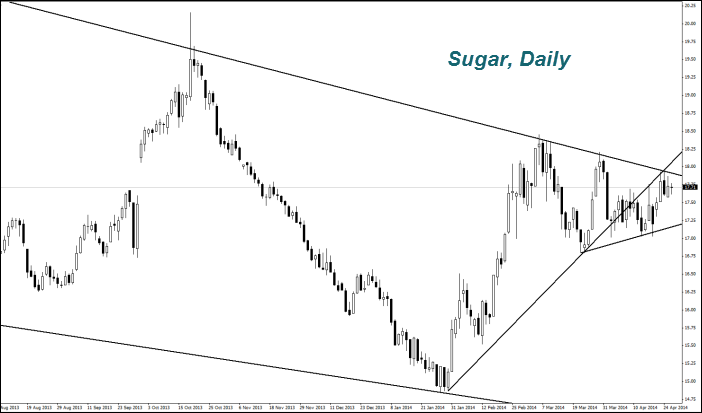

The Sugar prices increased slightly. The Brazilian company, Unica lowered its forecast for sugar cane harvest due to drought by 5% to 32.5 million tons. We do not exclude the increased volatility of futures contracts on sugar because of the nearest May contract redemption on the Intercontinental Exchange (ICE) next week. It has a lot of open positions. According to the U.S. Department of Agriculture (USDA), the number of cattle, located in the slaughterhouses in the U.S. unexpectedly fell in March by 5% compared to March 2013. Market participants were expecting it to be increased by 0.8%. Other indicators for cattle were also weak. This contributed to a further rise in the Fcattle prices. It was not really significant, as the quotes have grown by 8.5% since the beginning of this year and doubled since the beginning of 2010. This has contributed to a decline in the beef sales in the U.S. for March of this year by 4%, compared to the previous year, to the lowest level since 1996, when the USDA started to publish this information. We do not exclude a technical correction downwards. The Copper prices increased due to possible reduction in the Newmont Mining company production in Indonesia. The Indonesian Government is reviewing the copper export conditions, so it blocked its exports for now. Newmont Mining reported filling the warehouses and does not exclude the production decrease. The Wheat price has risen significantly because of the worsening political situation in Ukraine and possible sanctions against Russia. These two countries provide for about 17% of world grain exports. An additional factor in rising prices were the weather forecasts in the U.S. and reduced outlooks. This week, the drought may spread in half the territory of the American Great Plains that is a main wheat growing platform in the United States. The International Grains Council lowered its forecast for global maize and wheat production in the season 2014/15 to 950 million tons and 697 million tons respectively. Today at 21:00 CET, we will see the USDA report containing the data for spring planting of crops, which can affect the quotes.

The (Oil, Brent) prices rose due to the possible entry of additional sanctions against Russia (7th country in the world by oil reserves). We do not exclude further Oil and Gas (Natgas) appreciation. The Natural gas reserves in the U.S. fell to the lowest level of 11 years.

As we predicted in previous reviews, the Coffee prices corrected downwards. Earlier, its quotes have grown substantially due to lower crop forecast in Brazil because of the drought. Now the price movements are affected by the weather forecasts in this country. As in the case of the rain, the coffee harvest may be higher than the current market expectations. Brazil is the third Coffee producer in the world.

The Sugar prices increased slightly. The Brazilian company, Unica lowered its forecast for sugar cane harvest due to drought by 5% to 32.5 million tons. We do not exclude the increased volatility of futures contracts on sugar because of the nearest May contract redemption on the Intercontinental Exchange (ICE) next week. It has a lot of open positions. According to the U.S. Department of Agriculture (USDA), the number of cattle, located in the slaughterhouses in the U.S. unexpectedly fell in March by 5% compared to March 2013. Market participants were expecting it to be increased by 0.8%. Other indicators for cattle were also weak. This contributed to a further rise in the Fcattle prices. It was not really significant, as the quotes have grown by 8.5% since the beginning of this year and doubled since the beginning of 2010. This has contributed to a decline in the beef sales in the U.S. for March of this year by 4%, compared to the previous year, to the lowest level since 1996, when the USDA started to publish this information. We do not exclude a technical correction downwards. The Copper prices increased due to possible reduction in the Newmont Mining company production in Indonesia. The Indonesian Government is reviewing the copper export conditions, so it blocked its exports for now. Newmont Mining reported filling the warehouses and does not exclude the production decrease. The Wheat price has risen significantly because of the worsening political situation in Ukraine and possible sanctions against Russia. These two countries provide for about 17% of world grain exports. An additional factor in rising prices were the weather forecasts in the U.S. and reduced outlooks. This week, the drought may spread in half the territory of the American Great Plains that is a main wheat growing platform in the United States. The International Grains Council lowered its forecast for global maize and wheat production in the season 2014/15 to 950 million tons and 697 million tons respectively. Today at 21:00 CET, we will see the USDA report containing the data for spring planting of crops, which can affect the quotes.

News

Bitcoin at $67K: Key Levels, Technicals and What's Driving the Price

Bitcoin is in a later stage of post-halving cycle, meaning prices...

31/3/2026

Meta Analysis: Not Addiction

The lawsuit against Meta in California is a battle over semantics,...

27/3/2026

From ChatGPT to the Department of War

This situation is a classic example of corporate chess. By early...

26/3/2026

Private Market in 2026: Blue Owl Capital

In the past few months Blue Owl Capital stock prices fell impressively...

17/3/2026

Why FedEx is Suing US Government

On the surface FedEx’s recent lawsuit against the U.S. government...

13/3/2026

Explore our

Trading Conditions

- Spreads from 0.0 pip

- 30,000+ Trading Instruments

- Stop Out Level - Only 10%

Ready to Trade?

Open AccountSee Also

Follow the Market with Our Live Tools and Calendars

Market Analysis Lab from Our Top Experts