- Analytics

- Market Overview

S&P500 closed positively for the sixth day in a row - 23.6.2014

The world stock market had no single trend on Friday. The U.S. stocks rose in the absence of significant macroeconomic information. The S&P500 closed positively for the sixth day in a row and renewed its historical high once again. Moreover, the trading volume on the U.S. exchanges was 31% above the monthly average, making 7.2 billion shares.

Perhaps investors do not exclude the higher inflation continuation in the U.S. and believe that shares are more attractive than other assets in such circumstances. The Canadian CPI rise in May reached its highest level of 27 months and was 2.3% in annual terms. Recall that in the U.S. inflation rate in May was 2.1%. The June figure is not coming before July 22. We will see the Markit (PMI) at 13-45 СЕТ and the home sales in the secondary market at 14-00. In our opinion, the preliminary forecasts are positive. Now, the U.S. futures are traded "in the black".European stock indexes fell markedly today. Indexes of industrial and business activity for June in Germany, France and the EZ, were worse than the preliminary forecasts as a whole. Especially weak performance was shown by France. Thanks to this, the SAS40 collapsed to 2-week low. There is no important data expected from the EU for today.

Japanese Nikkei rose initially to 5-month high thanks to the good PMI performance for June in Japan and in the neighboring China. Moreover, the Chinese PMI from HSBC/Markit rose for the first time during six months that also triggered the rapid increase of commodity futures.

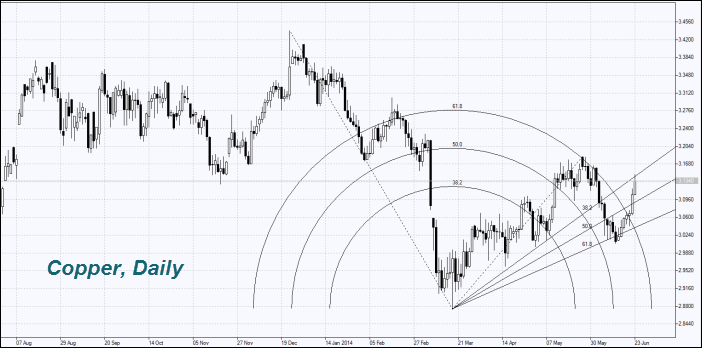

In particular, the Copper price has reached a maximum of three weeks. We noted an increase in the demand in our previous reviews, the quotes are rising seven days in a row. But the good data on Chinese industry growth that contributes to the reduction of its stocks on the London Metal Exchange by 850 tons to its lowest 6yrs level at 158, 5 thousand tons. And a ton of Copper in Shanghai reached $ 8 thousand, while in London it costs $ 6890. China exported 283 tons of copper in May, which is 21.9% higher than the last year, but 17% less than in April of this year. Note that according to the U.S. CFTC, the Copper formed the net short position for the first time since April. Indonesia may have exporting metal suspended in January. Two of the U.S. companies have the reduction of export duties from Indonesian government.

The Sugar prices rose. India plans to increase its import duties by 40%, not by15% as previously expected. So it wants to support the local farmers. Market participants believe that a part of the planned export volume estimated at 2 million tons can enter the domestic Indian market because of this.

The NATGAS price dropped. The US Energy Information Administration predicts an increase in its production in the U.S. by 4% for 2014, compared to last year. Meanwhile, according to the Gulf Coast Power Association, the GAS price at $ 4 per million British thermal units is too low for sustained growth in shale gas production. We do not exclude that this level can be a fundamental support on the NATGAS.

The SOYB and the grain futures keep rising amid rainy weather in the U.S. and the threat of flooding in some agricultural regions.

News

Bitcoin at $67K: Key Levels, Technicals and What's Driving the Price

Bitcoin is in a later stage of post-halving cycle, meaning prices...

Meta Analysis: Not Addiction

The lawsuit against Meta in California is a battle over semantics,...

From ChatGPT to the Department of War

This situation is a classic example of corporate chess. By early...

Private Market in 2026: Blue Owl Capital

In the past few months Blue Owl Capital stock prices fell impressively...

Why FedEx is Suing US Government

On the surface FedEx’s recent lawsuit against the U.S. government...

Explore our

Trading Conditions

- Spreads from 0.0 pip

- 30,000+ Trading Instruments

- Stop Out Level - Only 10%

Ready to Trade?

Open AccountSee Also