- Analytics

- Market Overview

The Dollar index yesterday fell due to Janet Yellen’s statement - 28.2.2014

The U.S. Dollar Index (USDIDX) dropped yesterday after the FED Chairman, Janet Yellen’s speech where it was said that her agency may continue to repurchase government bonds for a longer period than it is expected. According to investors, this implies a possible extension of smooth monetary policy with low interest rates. The main reason were the weak U.S. macroeconomic indicators. However Thursday data were not bad. The orders for durable goods,excluding transportation, unexpectedly increased in January by 1.1%. This is the most significant growth during last eight months that could have a positive impact on American industry. Yesterday's weekly unemployment figures were weaker than expected. However, they did not affect the market, as investors decided that employment fluctuations were caused by the large number of federal holidays in the beginning of the year and by unusual severe frosts. The support for the U.S. Dollar continues to come from weakening of the Yuan. Today it may be the biggest in recent years. The Bank of China carries out currency intervention to weaken the national currency before the cabinet meeting next week, where the further economic course will be discussed. Recall that on Saturday, China will release the Manufacturing PMI. The preliminary forecast is negative. This can affect the price of commodity futures and foreign exchange rates.

Today, the U.S. will release important macroeconomic information. More about this can be read in Economic Calendar section on our website. The (Q4) GDP data in the second reading at 13-30 GMT (0) may affect the Dollar. Its growth is expected to be revised to 2.5% after rising by 3.2% in the first reading. Accordingly, the greater the actual figure is, the better it is for the U.S. Dollar. Other data, which will be released later, may be neutral according to forecasts.

Today, at13-30 GMT (0) the Canadian GDP for December will be announced. The preliminary forecast is neutral. If it is not justified, it may cause a significant movement of the Canadian Dollar (USDCAD).

The weakening Yuan also helps strengthening the Japanese Yen (fall on the USDJPY chart). The second factor for the Yen, yesterday's movement were the macroeconomic data. Inflation in January rose to a five-year maximum and amounted to 1.4% on annualized basis. The industrial production increased by 4 % for the month. This is the most significant growth over the past four years. Unemployment remained at six-year low (3.7%). Of course, all this testifies in favor of significant exchange rate strengthening. However, Japanese government is struggling with this trend and conducts its redemption of government bonds by printing money in amount of 60 trn. Yen per year. Perhaps it will increase to 70 trn. Yen. The purpose of the Bank of Japan is to achieve the inflation rate (2%). Now it is difficult to say who will win, whether emission or economy. We believe that the Yen will maintain the neutral trend until April when the sales tax is to be raised from 5% to 8%. Now we can expect significant macroeconomic data from Japan to come out next week on Thursday and Friday. The Australian Dollar (AUDUSD) stabilized before the RBA meeting that is to be held on fourth of March. Investors believe that the discount rate will remain at the current level of 2.5% for the seventh time in a row. As we noted in the previous review, next week will bring a lot of Australian reports. There are the GDP data, Trade Balance and Retail Sales expected.

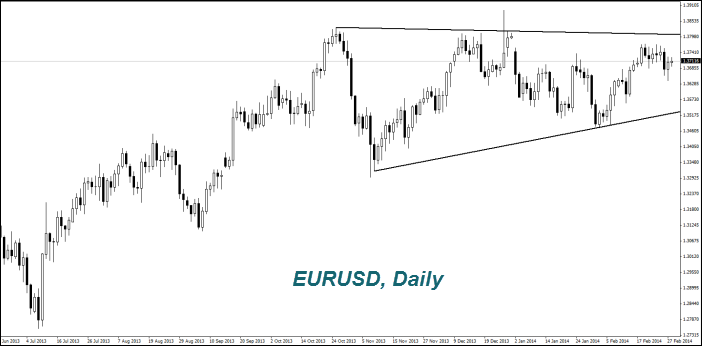

On Thursday, the strengthening of the Euro (rise on the EURUSD chart) was limited due to a sudden decrease in the harmonized German CPI for February to minimum of three and a half years (1%). Today at 10-00 GMT (0), there are the EZ inflation data expected to come out. According to forecasts, it will not change and will be at 0.8%. If the rise in consumer prices turns out lower, like in Germany, it will increase the likelihood of rate cuts by the ECB at next week meeting on Thursday. This will cause the fall of the Euro.

As it was expected in the previous overview, the USDA reported an increase in sales of soybean (Soyb) by 280% compared to the previous week. Sales of wheat (WHEAT) decreased by 14%. Note that the wheat price was also influenced by other factors that we have discussed in previous overviews.

The weakening Yuan also helps strengthening the Japanese Yen (fall on the USDJPY chart). The second factor for the Yen, yesterday's movement were the macroeconomic data. Inflation in January rose to a five-year maximum and amounted to 1.4% on annualized basis. The industrial production increased by 4 % for the month. This is the most significant growth over the past four years. Unemployment remained at six-year low (3.7%). Of course, all this testifies in favor of significant exchange rate strengthening. However, Japanese government is struggling with this trend and conducts its redemption of government bonds by printing money in amount of 60 trn. Yen per year. Perhaps it will increase to 70 trn. Yen. The purpose of the Bank of Japan is to achieve the inflation rate (2%). Now it is difficult to say who will win, whether emission or economy. We believe that the Yen will maintain the neutral trend until April when the sales tax is to be raised from 5% to 8%. Now we can expect significant macroeconomic data from Japan to come out next week on Thursday and Friday. The Australian Dollar (AUDUSD) stabilized before the RBA meeting that is to be held on fourth of March. Investors believe that the discount rate will remain at the current level of 2.5% for the seventh time in a row. As we noted in the previous review, next week will bring a lot of Australian reports. There are the GDP data, Trade Balance and Retail Sales expected.

On Thursday, the strengthening of the Euro (rise on the EURUSD chart) was limited due to a sudden decrease in the harmonized German CPI for February to minimum of three and a half years (1%). Today at 10-00 GMT (0), there are the EZ inflation data expected to come out. According to forecasts, it will not change and will be at 0.8%. If the rise in consumer prices turns out lower, like in Germany, it will increase the likelihood of rate cuts by the ECB at next week meeting on Thursday. This will cause the fall of the Euro.

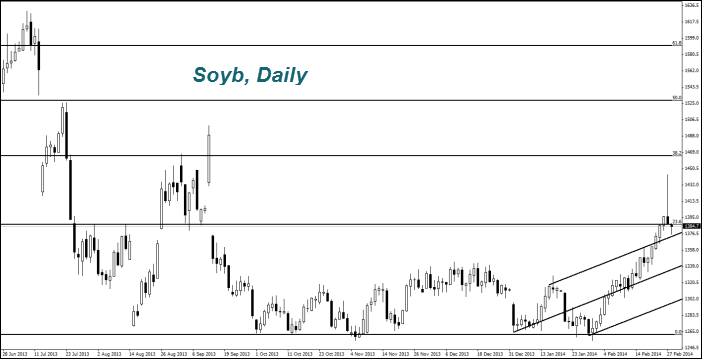

As it was expected in the previous overview, the USDA reported an increase in sales of soybean (Soyb) by 280% compared to the previous week. Sales of wheat (WHEAT) decreased by 14%. Note that the wheat price was also influenced by other factors that we have discussed in previous overviews.

News

META Lost $119 Billion in a Day

Structural bearish pressure is building up; two verdicts confirm...

3/4/2026

Bitcoin at $67K: Key Levels, Technicals and What's Driving the Price

Bitcoin is in a later stage of post-halving cycle, meaning prices...

31/3/2026

Meta Analysis: Not Addiction

The lawsuit against Meta in California is a battle over semantics,...

27/3/2026

From ChatGPT to the Department of War

This situation is a classic example of corporate chess. By early...

26/3/2026

Private Market in 2026: Blue Owl Capital

In the past few months Blue Owl Capital stock prices fell impressively...

17/3/2026

Explore our

Trading Conditions

- Spreads from 0.0 pip

- 30,000+ Trading Instruments

- Stop Out Level - Only 10%

Ready to Trade?

Open AccountSee Also

Follow the Market with Our Live Tools and Calendars

Market Analysis Lab from Our Top Experts