- Analytics

- Market Overview

Investors expect the Bank of England and the ECB meetings, as well as tomorrow's data on the U.S. labor market - 6.2.2014

There was relatively quiet trading in the Forex market yesterday. The Macroeconomic data from the U.S. compensated for each other, so the Dollar Index (USDIDX) has not changed. As it was expected, the labor market report from ADP was negative, while the index of business activity in the service sector was on the contrary positive. Today we expect: the unemployment for the week and the trade balance for December from the U.S. at 13-30 GMT (0). In our opinion, the preliminary forecast in general is positive. However, this information is not the main one.

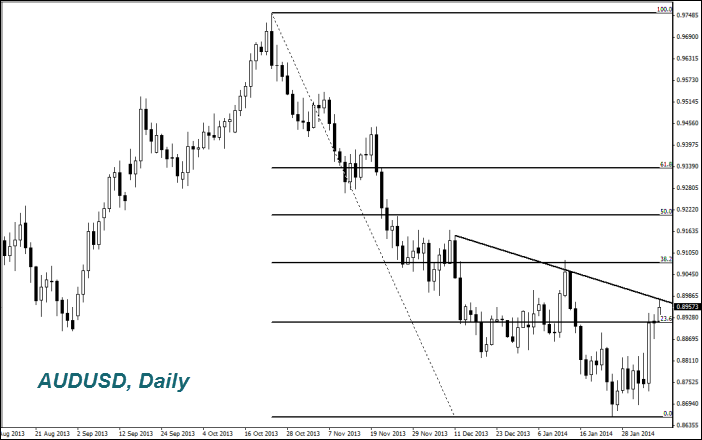

Investors expect today's meeting of the Bank of England at 12-00 GMT (0) and the ECB meeting at 12-45 GMT (0), as well as the data on the U.S. labor market on Friday. Most of market participants believe that the Bank of England will keep interest rates at the current level (0.5%). As for the ECB, the opinion was divided. It may keep or slightly lower its discount rate. We believe that if the rate does not change, the euro (EURUSD) can jump up and then can be corrected. Accordingly, in case of rate cut the opposite reaction is possible. The PMI in the service sector in the UK for December was worse than the preliminary forecasts. It dropped to the lowest level since June. However, the weakening of the Pound (falling on the chart) (GBPUSD) was not too sharp. Market participants expect the Bank of England to make a number of positive statements after the decision on the discount rate. In addition, the UK will release several key economic indicators tomorrow. Tonight the unexpectedly good statistics came out in Australia. The trade balance surplus was the highest in two years. Contrary to talks about slowing in the Chinese economy, exports of raw materials from Australia to China in 2013 grew by 29% to A $ 94 billion ($ 85 billion). The macroeconomic data have strengthened the Australian Dollar (AUDUSD) (growth on the chart). Market participants believe that the indicators reduce the likelihood of further reduction in interest rates.

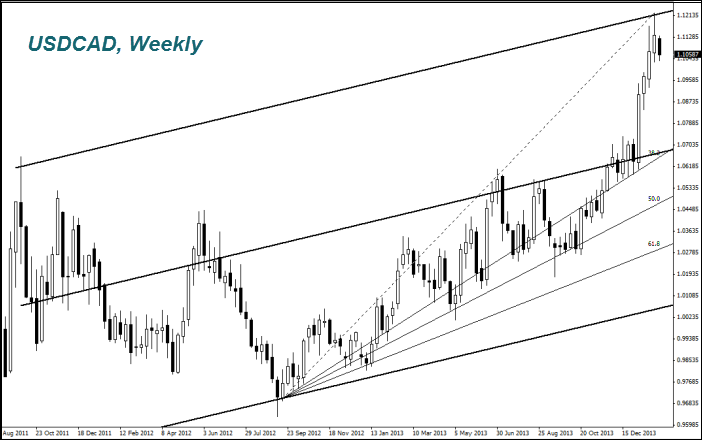

The Canadian Dollar (USDCAD) has been corrected down after a sharp rise in January. This means strengthening of it, which continued in spite of yesterday unexpectedly weak data on the real estate market. The number of building permits in Canada declined in December for the second month in a row and was the lowest since March 2013. Today at 15-00 GMT (0) we expect the Purchasing Managers' Index for January to be released. The preliminary forecast is positive for the Canadian Dollar. If it is justified, the CAD may continue to move lower. The more important data (on the labor market in Canada) are expected tomorrow. As we anticipated in yesterday's review the rise in wheat (WHEAT) and natural gas (NATGAS) continued. From the beginning, the gas price increased by 22% and the price refreshed its maximum of five years yesterday with low trading volumes. Recall that today at 15-30 GMT (0) we expect the report on the gas reserves in the United States for the week. They are expected to be 23% below last year's level. This can improve the gas quotations. The increase in wheat prices helped Japanese decision to increase its purchases in the United States. Since the delivery of Canadian wheat to Japan has been delayed due to bad weather in Canada. Market participants expect the wheat prices to a rise to $ 600-610.

Investors expect today's meeting of the Bank of England at 12-00 GMT (0) and the ECB meeting at 12-45 GMT (0), as well as the data on the U.S. labor market on Friday. Most of market participants believe that the Bank of England will keep interest rates at the current level (0.5%). As for the ECB, the opinion was divided. It may keep or slightly lower its discount rate. We believe that if the rate does not change, the euro (EURUSD) can jump up and then can be corrected. Accordingly, in case of rate cut the opposite reaction is possible. The PMI in the service sector in the UK for December was worse than the preliminary forecasts. It dropped to the lowest level since June. However, the weakening of the Pound (falling on the chart) (GBPUSD) was not too sharp. Market participants expect the Bank of England to make a number of positive statements after the decision on the discount rate. In addition, the UK will release several key economic indicators tomorrow. Tonight the unexpectedly good statistics came out in Australia. The trade balance surplus was the highest in two years. Contrary to talks about slowing in the Chinese economy, exports of raw materials from Australia to China in 2013 grew by 29% to A $ 94 billion ($ 85 billion). The macroeconomic data have strengthened the Australian Dollar (AUDUSD) (growth on the chart). Market participants believe that the indicators reduce the likelihood of further reduction in interest rates.

The Canadian Dollar (USDCAD) has been corrected down after a sharp rise in January. This means strengthening of it, which continued in spite of yesterday unexpectedly weak data on the real estate market. The number of building permits in Canada declined in December for the second month in a row and was the lowest since March 2013. Today at 15-00 GMT (0) we expect the Purchasing Managers' Index for January to be released. The preliminary forecast is positive for the Canadian Dollar. If it is justified, the CAD may continue to move lower. The more important data (on the labor market in Canada) are expected tomorrow. As we anticipated in yesterday's review the rise in wheat (WHEAT) and natural gas (NATGAS) continued. From the beginning, the gas price increased by 22% and the price refreshed its maximum of five years yesterday with low trading volumes. Recall that today at 15-30 GMT (0) we expect the report on the gas reserves in the United States for the week. They are expected to be 23% below last year's level. This can improve the gas quotations. The increase in wheat prices helped Japanese decision to increase its purchases in the United States. Since the delivery of Canadian wheat to Japan has been delayed due to bad weather in Canada. Market participants expect the wheat prices to a rise to $ 600-610.

- Get Certificate

See Also

Follow the Market with Our Live Tools and Calendars

Market Analysis Lab from Our Top Experts