- Analytics

- Market Overview

The European economic data that is more important than the data from the U.S. strikes out today - 6.5.2014

The U.S. Dollar has not changed on Monday, and has not responded to the growth in the index of business activity in the service sector (ISM) for April to a maximum of eight months (55.2 points). In our opinion, the U.S. Dollar Index (USDIDX) does not grow as investors do not expect a rate hike in the foreseeable future. Today we will see the U.S. trade balance released at 12-30 for March. The forecast is moderately positive.

There will be more important economic information released in Europe today. At 8-30 CET, we will find out about the business activity indexes - the composite index and in the service sector index for April. At 9-00 CET, we will see the data on retail sales in March. In our opinion, the preliminary forecasts are positive. Note that the interbank overnight rates sometimes exceed the ECB rate for the first time since 2008. In our opinion, this reflects the lack of liquidity and may contribute to the monetary policy easing in the future.

At 12-30 and 14-00 CET we will see the Canadian economic data such as: the trade balance for March and the PMI (Ivey) for April. The forecast is neutral. However, the trade balance data can affect the Canadian Dollar (USDCAD), if it significantly deviates from the expectations of investors. The following important information on the Canadian labor market will be released on Friday.

The Australian Dollar (AUDUSD) rose upto 2-week high after the RBA meeting. The discount rate has not changed. The RBA noted positive trends in the labor market. Tomorrow night at 1-30 CET we will see the Australian retail sales data for March and the first quarter. In our opinion, the preliminary forecast is positive.

Japanese financial markets did not work this morning because of the holiday (the Children’s Day). At 23-50 night time, we will see the BOJ meeting minutes that may affect the Yen.

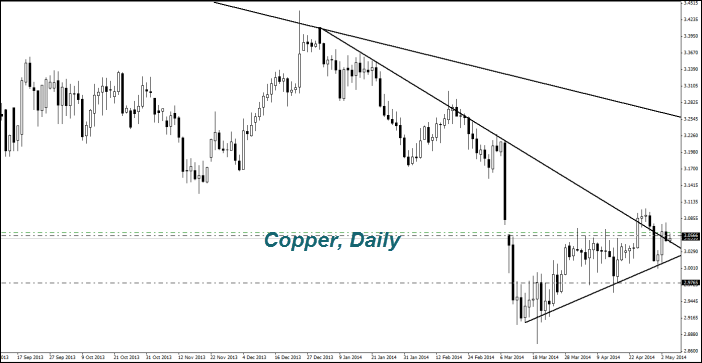

The (Copper) was corrected slightly down due to the message from Glencore Xstrata about increase this metal production by 24% in the first quarter to 382 thousand tons. The company launched the new mines in Africa, Australia and South America.

The (Wheat) prices continued to rise. Yesterday, after the market was closed, U.S. Department of Agriculture (USDA) has reduced the assessment of the quality winter wheat planting by 2% compared to the previous week to 31% (good and excellent). This is the lowest level since 1996. The other important factors of the increase in prices are the drought in the United States and the political situation in Ukraine. On May 9 at 20-00 CET, the USDA will publish its crop forecast for all major crops for the current season.

The (Coffee) prices are in a neutral trend. The Vietnamese market was closed from April 30 to May 4, due to the holidays. The projected coffee export from Vietnam in May could be reduced to 150-220 thousand tons from 220 thousand tons in April. Its price grows and Vietnamese farmers are reluctant to sell it, waiting for even higher prices. Now the country has about 40% of the previous coffee harvest, or about 10 million bags (60 kg). We do not exclude that this volume will keep prices in a neutral trend. A Part of the reserves probably began to arrive on the world market. Since the discount on Vietnamese coffee to the price of the July futures in London widened to $60-90 from $85 per ton last week.

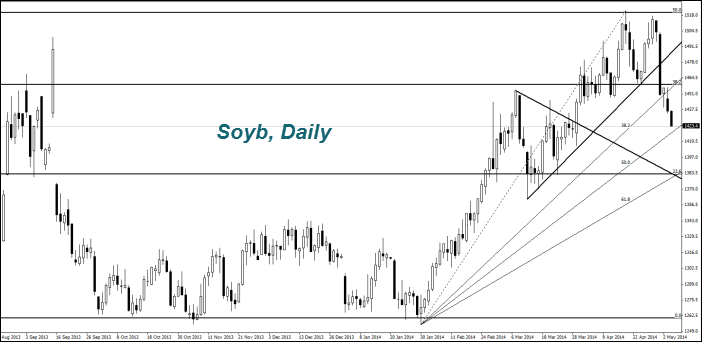

The (Corn) and the (Soyb) prices go lower in spite of the low planting volume in the United States. There was 29% of corn planted on May 4, which is below the predictions (33%). The medium level of 5 years on this date is 42%. Planting soybeans amounted to 5% with the forecast of 8%. The medium level of 5 years on that date for soybeans is 11%. The schedule delay is due to bad weather conditions. As we have mentioned in previous reviews, a noticeable drop in soybean prices caused by the reduction in its imports to China because of the poultry death due to the outbreak of avian influenza. Soybean imports to China amounted to 6.5 million tons in April. Though 6.9 million tons were expected. According to the forecasts, it will be reduced to 4.85 million tons in May.

News

China-Us Supply Chain Competition

China added 10 more American companies to its entities list and...

Is Bitcoin Price Recovery Real or Just a Temporary Bounce

Bitcoin dropped sharply through early 2026, falling to around...

Trading Gold (XAUUSD) Under the New Fed Chair

Kevin Warsh is taking over the Federal Reserve with a clear mission...

FedEx Sues Brooklyn Law Firm Over Fake Accident Claims

FedEx moves nearly everything Americans buy, from groceries to...

30-year Treasury yield has crossed 5%

The 30-year Treasury yield has crossed 5% , let’s see who pays...

Oil Price Analysis 2026 May

WTI crude futures fell below the $93 per barrel mark this morning,...

Explore our

Trading Conditions

- Spreads from 0.0 pip

- 30,000+ Trading Instruments

- Stop Out Level - Only 10%

Ready to Trade?

Open AccountSee Also