- Analytics

- Market Overview

Fed chairman Janet Yellen stated about maintaining the policy of low interest rates - 8.5.2014

The U.S. Dollar Index (USDIDX) has not changed on Wednesday. As it was expected, the Fed chairman Janet Yellen said yesterday about maintaining the policy of low interest rates for a long time even after the QE is over. The policy conditions are low inflation and weak labor market data. In our opinion, this means that the Fed will consider the possibility of increasing the discount rate only in the case of significant inflation increase above the target level of 2%. The unemployment level for April has dropped below 6.5%, the target previously set by the Fed. In this regard, the USD exchange rate can affect the inflation data for April, which will be released next Thursday. Today at 13-30 CET we will see the information appeared regarding the labor market for this week. In our opinion, the preliminary forecast is positive.

According to Reuters, most of the major investors believe that if the Euro (EURUSD) reaches 1,42-1,45 USD, the European Central Bank will continue the monetary policy easing aimed at the single currency weakening. Such a step can be expressed in the form of reduced rates or the EUR emission. Note that during the last 6 months, the Euro rose by 4%. Today at 12-45 CET we expect the ECB meeting and the Bank of England meeting at 12-00 CET. There are no changes in interest rates of 0.25% and 0.5%, respectively expected in conclusion. According to market participants, Great Britain could become the second of the developed countries in the future , who raises interest rates after New Zealand. At 13-30 CET, the ECB President, Mario Draghi will speak at the press conference for journalists and investors.

The Australian Dollar (AUDUSD) continues to grow this morning, thanks to the good labor market data and positive economic data from China for April. Unemployment in Australia for March remained at 5.8%, slightly better than expected. China announced an increase in the trade surplus to $7.7B in March to $18.46B.

The Wheat prices began the downward correction after the strong growth. Investors reacted to the cessation of hostilities in the South-East of Ukraine. They believe that the normalization of the political situation may increase the export of Ukrainian grain. We do not expect any strong price movements before the first official forecast of wheat crop in the season 2014/2015 from the U.S. Department of Agriculture coming out tomorrow.

The Soyb prices increased due to the post of growth in its imports to China in April to 6.5 million tons compared to 4.6 million tons in March and 4 million tons in April last year. The increased demand is due to the poultry recovery after avian influenza H7N9. The Soyb is an important component of the feed used by poultry farms. Now market participants expect China to import 6 million tons of beans in May and June.

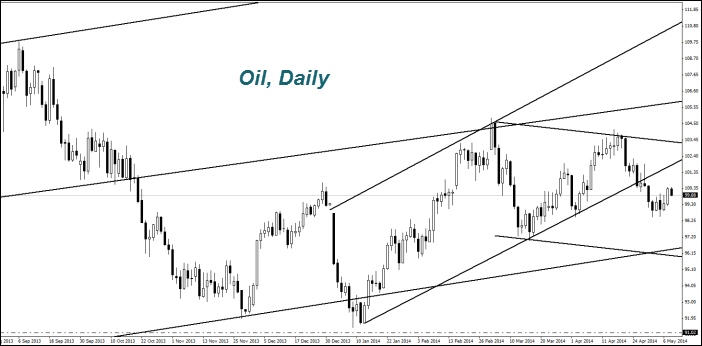

The Oil (Brent) has risen after reports of increase of its imports to China in April to 6.78 million barrels a day from 5.54 million in March. Chinese oil imports grew in January-April 2014 by 11.5% compared to the same period last year. An additional factor of the price growth was the decrease of stocks in the U.S. last week by 1.4 million barrels, and the resumption of hostilities in Libya. The Oil exports from the African country remains at the low level of 250 thousand barrels per day, compared with 1.4 million barrels per day in the middle of 2013.

The price fell yesterday. Meanwhile, China reported an increase in its imports in April by 7.2% compared to March. In comparison to April of the last year its purchases rose by 52%. Note that compared to the level for the beginning of the year, the world Copper prices are still below 9%.

News

China-Us Supply Chain Competition

China added 10 more American companies to its entities list and...

Is Bitcoin Price Recovery Real or Just a Temporary Bounce

Bitcoin dropped sharply through early 2026, falling to around...

Trading Gold (XAUUSD) Under the New Fed Chair

Kevin Warsh is taking over the Federal Reserve with a clear mission...

FedEx Sues Brooklyn Law Firm Over Fake Accident Claims

FedEx moves nearly everything Americans buy, from groceries to...

30-year Treasury yield has crossed 5%

The 30-year Treasury yield has crossed 5% , let’s see who pays...

Oil Price Analysis 2026 May

WTI crude futures fell below the $93 per barrel mark this morning,...

Explore our

Trading Conditions

- Spreads from 0.0 pip

- 30,000+ Trading Instruments

- Stop Out Level - Only 10%

Ready to Trade?

Open AccountSee Also