- Analytics

- Market Overview

World stock indices downward correction on Tuesday, after 2-day growth - 13.8.2014

World stock indices showed a slight downward correction on Tuesday, after the 2-day growth. We pointed out the reduced volume of trading on the American stock exchanges in the previous overviews. As a rule, it can indicate unsustainable price movements, thus the correction was quite expected.

By the way, the US volume of trading slumped even more to the monthly low and amounted to 4.3 billion stocks. Market participants are not in a hurry to trade in the absence of fresh economic data. American data was not released for 2 days. In our opinion, the main economic event of this week is to happen today: Retail Sales for July is to be published at 12-30 CET. It is expected to be increased for the sixth consecutive month, which can be considered as a positive factor. Moreover, Business inventories are to be released at 14-00 CET. Currently futures on American stock indices are being traded “in the black”. Investors are looking forward to the policy environment in Ukraine to be less tense. Russia sent the convoy of about three hundred trucks with humanitarian aid.

Yesterday, European indices decline was more prominent than the American ones, due to weak German economic indicators calculated by The Centre for European Economic Research (ZEW). The EU stock prices are rising today, due to the partial stabilization in Ukraine and good quarterly financial statements of the insurance company Swiss Life and LCD screens manufacturer Merck. Industrial production in the Eurozone is to be announced at 9-00 CET. We assume that the preliminary forecasts are moderately negative. The Bank of England published the Inflation Report at 9-30 CET. Stoxx Europe 600 P/E ratio fell to 14.9 from 15.7 in July. Now investors expect the increase in total profits of the companies listed in the index by 7.5% in 2014. It is almost twice lower than the January forecast of +14%.

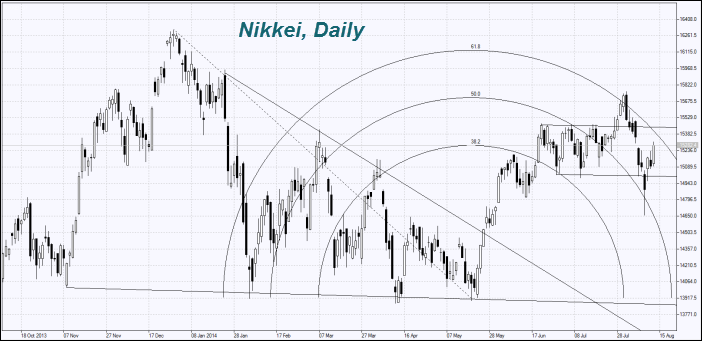

Nikkei has risen considerably this morning at a modest volume of trading, 18% lower than the month average. A few positive factors contributed to this fact. The GDP drop in the second quarter made up -6.8%, and occurred to be less than the forecast of -7.1%. The Bank of Japan announced the continuation of the economy stimulation policy and did not rule out its increase, which resulted in the yen depreciation. The Prime Minister of Japan Shinzo Abe said, the sales tax increase from 8% to 10%, scheduled for October of the next year, is still to be discussed. The weekly data on the investment activity and factory orders for June is to be released tonight at 23-50 CET by the Japanese Ministry of Finance. The outlook appears to be positive. Investors count on the stock market support, due to purchases of the Japanese government fund, which previously announced the plans to raise its stake in the portfolio.

Another piece of Chinese statistics has come out this morning. Industrial production, retail sales and the volume of yuan loans appeared to be worse than the preliminary forecasts. The economic slowdown in China may affect commodity futures quotes. In particular, for this reason copper and oil prices have tumbled today.

The US oil extraction rose 3 million barrels per day (bpd) since 2008, and reached the 27-year high. Due to this, oil imports into the United States dropped by more than a quarter since 2008 and makes up 7.17 million bpd. Its share in the total consumption fell to the lowest point in 1970 and is equal to 22%. We note that the U.S. consumes about a third of the world oil produced. Therefore, the changes in the American demand have a significant impact on the oil price. Brent oil price dropped to the 13-month low.

A record high corn crop in the United States is expected, 14.03 billion bushels this year, according to USDA forecast. However, this is below the forecast level of market participants, 14.25 billion. The volume of corn inventories at the end of the season could reach 1.8 billion bushels, which is also less than the market had expected. A similar situation with soybean forecasts was reported. Due to this, these commodity futures prices remained almost unchanged after the monthly USDA report release.

USDA has cut the US sugar supply forecast. As a result, the predicted stock to use ratio fell to the lowest level since April 2012 and made up 6.9% versus 14.1% last year. Let us remind you that the U.S. anti-dumping measures for Mexican sugar were enforced. After that, Mexico was redirected to other demanders. We do not discard that the USDA forecast can provide support for sugar prices.

News

Three Things Moving Markets This Week

There's a lot going on in the world economy right now, American...

Inside Paramount’s $111 Billion Deal Pause

When Paramount Skydance announced it was putting its massive...

What the Oil Price Drop Really Means

Oil prices took a sharp drop on Sunday evening 5 % after the...

China-Us Supply Chain Competition

China added 10 more American companies to its entities list and...

Is Bitcoin Price Recovery Real or Just a Temporary Bounce

Bitcoin dropped sharply through early 2026, falling to around...

Trading Gold (XAUUSD) Under the New Fed Chair

Kevin Warsh is taking over the Federal Reserve with a clear mission...

Explore our

Trading Conditions

- Spreads from 0.0 pip

- 30,000+ Trading Instruments

- Stop Out Level - Only 10%

Ready to Trade?

Open AccountSee Also