- Analytics

- Market Overview

The Fed's decision nevertheless supported the dollar - 31.1.2014

As we anticipated in yesterday report, the Fed's decision nevertheless supported the dollar. In addition, the macroeconomic data were slightly worse than expected, but nevertheless they confirmed the positive trends in the U.S. economy. The GDP in the fourth quarter increased by 3.2 % per annum. Its cumulative growth for the second half of last year was 3.7%. This is the maximum increase in the second half of 2003. In the first half of 2013, the GDP increased only by 1.8%. The rest of yesterday economic data in the U.S. were relatively weak, but the market ignored them.

Macroeconomic information from the EU lead to the weakening of the Euro. The unified German consumer price index for January was released yesterday. Its growth of 1.2% was lower than expected. Forex market participants now expect inflation across the EU to reach 0.8 % instead of 0.9 % as previously expected. In this case, the deflation risk for the European economy will be increased. To prevent it, the ECB may weaken the monetary policy in any way on the basis of its meeting on February 6th. Recall that according to the ECB plans, the consumer price index in the Eurozone should approach 2% by 2015. The inflation data in the EU in January will be released today at 10-00 GMT (0). Besides it, the unemployment rate will be known. It is projected to be unchanged at 12.1%. In general, the data for the Euro is more negative then vice versa. This morning, it continues to decline. Today at 13-30, 14-00, 14-45 and 14-55 GMT (0), we expect the U.S. macroeconomic data. In our opinion they are able to affect the U.S. dollar exchange rate in case of significant deviation from actual values from their neutral preliminary forecasts. The Personal Spending data may be the most important event.

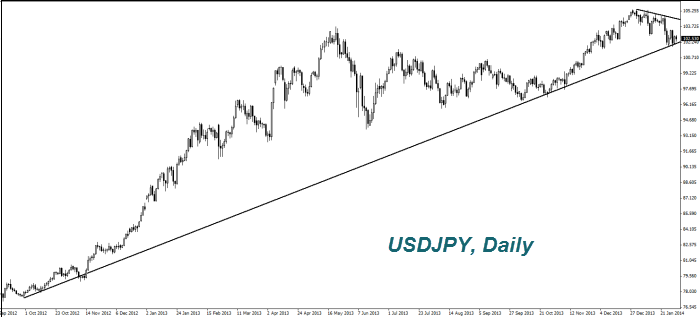

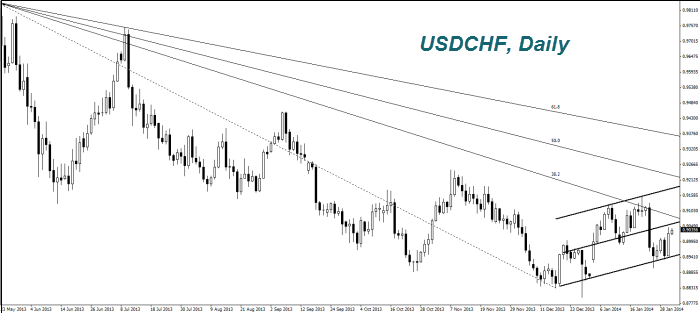

Low inflation data for Japan in December were released last night. It rose to a peak in the last five years at 1.6 % on an annualized basis. Nevertheless, strengthening of the Yen (USDJPY) (fall in the chart) now is not very sharp. The Bank of Japan stated that the Yen strengthened anyway by 2.5% for the first time in six months of weakening. In the BOJ point of view, the macroeconomic information is already included in the current rate. We, in turn, believe that the Japanese currency is likely to be in a neutral trend until April. You can read more about this in our previous reviews. However, if the increase in the sales tax, as well as steps by the Bank of Japan bring the expected effect, we can not exclude a further weakening of the Yen (continued growth in the chart) in the current year to around 110. We do not exclude that the Swiss Franc (USDCHF) can follow the Yen (growth in the chart ). Because both of these currencies are actively used in operations curry trade.

The Australian Dollar (AUDUSD) rose slightly (growth in the chart) on stopping the panic sales in the foreign exchange markets of developing countries and it should be noted that many investors do not preclude their recurrence in the future because of the Fed's steps in the market of U.S. government bonds. As we have mentioned, now “Aussie" is considered by major funds as a liquid analogue of currencies of developing market. Representatives of funds believe that his price may drop to 0.84. Next week on Monday in 00-30 GMT (0)/ we expect the real estate market and there are important macroeconomic data for Australia coming out on Thursday. Today at 13-30 GMT (0), we expect the Canadian GDP for November to be released. In our opinion, the preliminary forecast is neutral. However, the Canadian Dollar has fallen by 5% since the beginning of 2014 (growth in the chart). If the GDP grows is more than expected 2.6% per annum or 0.2% per month, then we can not exclude Loonie strengthening (downward correction in the chart).

The price of Cold (XAUUSD) decreased on the economic growth in the United States. As we have noted in their reviews, the Gold is regarded by investors as a defensive asset. It is more expensive in case of deterioration of the economic situation in the world. An additional negative factor for Gold has been the decline in its sales in China because of the weekend during the celebration of the Lunar New Year, which will last from today until February sixth. Now the premium to the Gold price in China compared to London fell to $ 4 per ounce compared to $ 20 at the beginning of the year. Investors do not exclude the Gold price decline to $ 1,200 per ounce.

The Australian Dollar (AUDUSD) rose slightly (growth in the chart) on stopping the panic sales in the foreign exchange markets of developing countries and it should be noted that many investors do not preclude their recurrence in the future because of the Fed's steps in the market of U.S. government bonds. As we have mentioned, now “Aussie" is considered by major funds as a liquid analogue of currencies of developing market. Representatives of funds believe that his price may drop to 0.84. Next week on Monday in 00-30 GMT (0)/ we expect the real estate market and there are important macroeconomic data for Australia coming out on Thursday. Today at 13-30 GMT (0), we expect the Canadian GDP for November to be released. In our opinion, the preliminary forecast is neutral. However, the Canadian Dollar has fallen by 5% since the beginning of 2014 (growth in the chart). If the GDP grows is more than expected 2.6% per annum or 0.2% per month, then we can not exclude Loonie strengthening (downward correction in the chart).

The price of Cold (XAUUSD) decreased on the economic growth in the United States. As we have noted in their reviews, the Gold is regarded by investors as a defensive asset. It is more expensive in case of deterioration of the economic situation in the world. An additional negative factor for Gold has been the decline in its sales in China because of the weekend during the celebration of the Lunar New Year, which will last from today until February sixth. Now the premium to the Gold price in China compared to London fell to $ 4 per ounce compared to $ 20 at the beginning of the year. Investors do not exclude the Gold price decline to $ 1,200 per ounce.

News

Bitcoin at $67K: Key Levels, Technicals and What's Driving the Price

Bitcoin is in a later stage of post-halving cycle, meaning prices...

31/3/2026

Meta Analysis: Not Addiction

The lawsuit against Meta in California is a battle over semantics,...

27/3/2026

From ChatGPT to the Department of War

This situation is a classic example of corporate chess. By early...

26/3/2026

Private Market in 2026: Blue Owl Capital

In the past few months Blue Owl Capital stock prices fell impressively...

17/3/2026

Why FedEx is Suing US Government

On the surface FedEx’s recent lawsuit against the U.S. government...

13/3/2026

Explore our

Trading Conditions

- Spreads from 0.0 pip

- 30,000+ Trading Instruments

- Stop Out Level - Only 10%

Ready to Trade?

Open AccountSee Also

Follow the Market with Our Live Tools and Calendars

Market Analysis Lab from Our Top Experts