- Analytics

- Market Overview

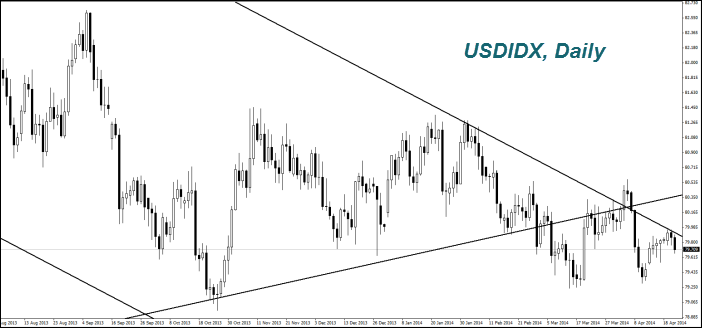

The negative impact of secondary real estate marketlower sales in in the United States will most likely limited - 23.4.2014

Yesterday's economic data in the EZ were neutral. Today, market participants' attention is focused on the manufacturing PMI for April, coming out at 10-00 CET. The forecast is neutral. We do not expect any powerful movements of the Euro (EURUSD). Since investors will most likely wait for tomorrow's speech of the ECB President.

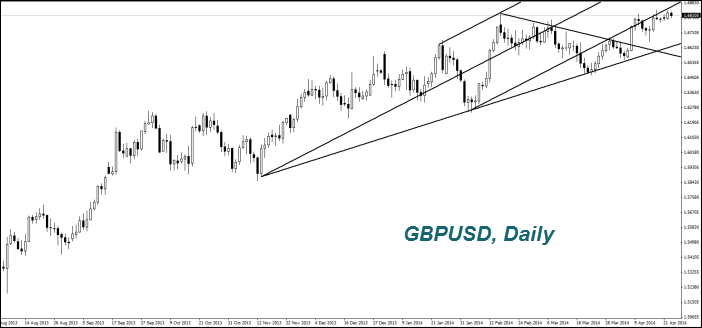

The British Pound (GBPUSD) strengthened slightly yesterday due to corporate news. British pharmaceutical company, GlaxoSmithKline sells some of its patents on cure for cancer to the Swiss company (Novartis) for $14.5B, when it buys production patents on several vaccines for $7.1B from Novartis. It is expected that the difference will be converted into the GBP. Earlier, the British telecommunications holding - Vodafone sold a part of its business and also converted Pounds into Dollars. The Pound slightly reduced (weakened) this morning, before the BOE report from its last meeting (Minutes), which will be released at 9:30 CET. Market participants doubt that the bank will raise interest rates before the parliamentary elections in May next year. Previously it was assumed that this can be done in the first half of 2015.

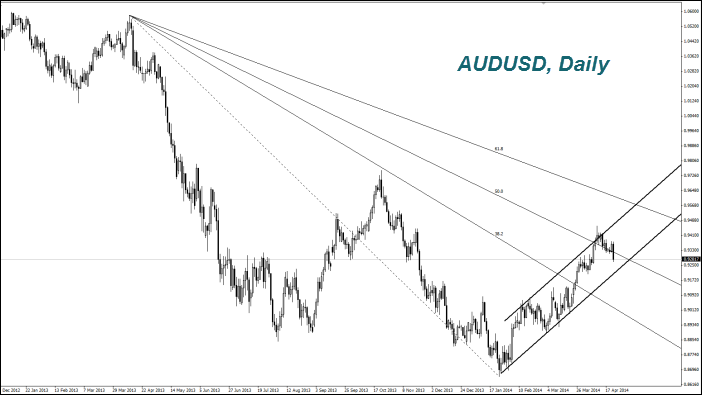

The Australian Dollar (AUDUSD) dropped markedly yesterday (weakening in the chart) after the CPI for the first quarter fell less than expected. Investors believe that it reduces the rate hike likelihood. Today, the Reserve Bank of New Zealand is going to increase the discount rate to 3% from 2.75%. We do not exclude that it may have a short-term positive impact on the New Zealand and Australian currencies. Chinese PMI for April rose slightly from 48 to 48.3 points and has not had a major impact on commodity futures. The Soyb prices continued to decline. As we have mentioned in previous reviews, the negative factor was China's abandonment of previously concluded contracts for supply of beans due to the recent outbreak of avian influenza. A few days ago, the U.S. and Japan bought Brazilian soybean, originally intended for China. However, according to investors its surplus still may be seen in the global market. An additional negative factor was the increase in the soybean forecast from the Rosario Grains Exchange for the harvest in Argentina by 200 thousand tons to 54.9 million tons. The Wheat prices rose after the Australian government has lowered its forecast for the crop this year to 24.8 million tons compared to 27.8 million tonnes for last year. Moreover, such a negative outlook is granted despite the increase of wheat acreage by 3.3 million acres this year. Australian Government experts explained it with expectations of El Nino in July, which may cause a serious drought on the eastern coast of the country. Note that the news about the slowdown in maize (Corn) planting in the U.S., which we wrote in the previous review, provoked a good price growth yesterday. Since there are many reviews from different companies, dedicated to the USDA data, which had a negative view regarding this year's harvest.

News

Inside Paramount’s $111 Billion Deal Pause

When Paramount Skydance announced it was putting its massive...

What the Oil Price Drop Really Means

Oil prices took a sharp drop on Sunday evening 5 % after the...

China-Us Supply Chain Competition

China added 10 more American companies to its entities list and...

Is Bitcoin Price Recovery Real or Just a Temporary Bounce

Bitcoin dropped sharply through early 2026, falling to around...

Trading Gold (XAUUSD) Under the New Fed Chair

Kevin Warsh is taking over the Federal Reserve with a clear mission...

FedEx Sues Brooklyn Law Firm Over Fake Accident Claims

FedEx moves nearly everything Americans buy, from groceries to...

Explore our

Trading Conditions

- Spreads from 0.0 pip

- 30,000+ Trading Instruments

- Stop Out Level - Only 10%

Ready to Trade?

Open AccountSee Also