- Analytics

- Market Overview

This day will be full of economic indicators - 30.4.2014

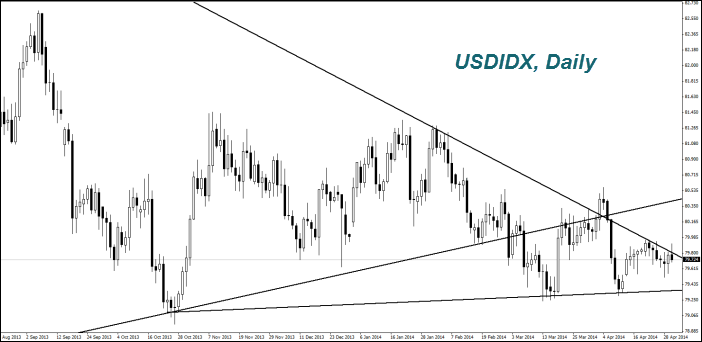

Inflation in Germany for April unexpectedly fell on Tuesday. This increases the likelihood of its decline in the entire EZ. The data will be released today at 11:00 CET. If the rise in consumer prices turns out less than the expected 0.8%, the ECB may announce the monetary easing already on May 8, during its next meeting. This is a negative factor for the Euro (EURUSD). Note that later, during the day, we will see the Retail Sales and Unemployment rate for individual European countries. Those data may increase the EUR volatility. This day will be full of economic indicators. The first data are the labor market report for April from the ADP coming out at 14-15. It precedes the official data, which will be announced on Friday. At 14-30, we will see the preliminary GDP announce for the first quarter. The University of Michigan manufacturing index will be released at 15-45. At the end of the day, at 20-00, the Fed will announce the monetary policy settings. The reduction in monthly redemption of government bonds for another $10 billion to $45 billion in our opinion is expected, all the preliminary forecasts are positive for the U.S. Dollar. The Bank of Japan kept its monetary policy unchanged, which caused a slight strengthening of the Japanese Yen (USDJPY). The volume of annual emissions will continue to be at 60-70 trn. Yen per year until inflation reaches 2%. It was 1.3% in March. Investors feared the increase in emissions. Now they believe that it could happen not earlier than July. Today's economic indicators were negative, which may limit the JPY growth (decrease in the chart). The next important data will be released in Japan in the morning on May 2 – the unemployment rate for March. The UK GDP growth in the first quarter was 3.1%. This is less than expected, but it is a maximum of the mid-2007. Investors could not decide how to respond to such statistics and the Pound (GBPUSD) has not changed. Tomorrow at 8-00 to 10-30 CET, we will see the economic information about the UK housing market and the PMI manufacturing index. The main event of the next days will be the Bank of England meeting on May 8th.

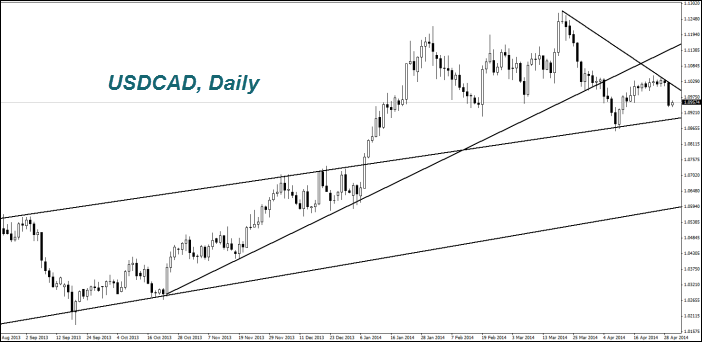

Yesterday strengthening of the Canadian Dollar (USDCAD) was caused by the positive statements from the Bank of Canada Chairman, Stephen Poloz about the economic state. Investors expect that the GDP for February may be better than expected. It will be released today at 14-30 CET.

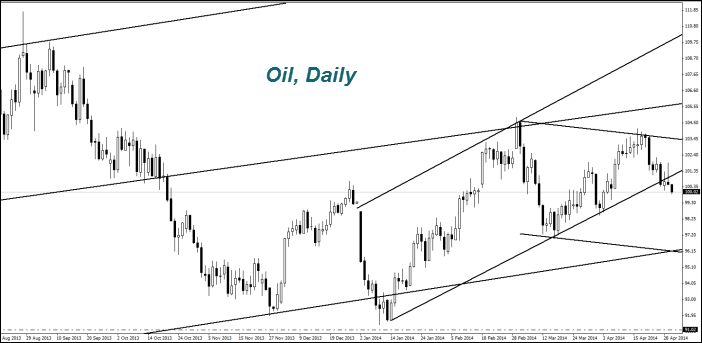

The Oil prices fell on expectations of growth in its stocks in the U.S. last week by 2.4 million barrels to 400 million barrels. This is the highest level since the beginning of publishing these data in 1982. The information about U.S. stocks will be released today at 16:30 CET. The additional factor of decline in the world Oil prices has been the increase of exports from Libya. If the market downtrend remains the same until the end of the day, the drop in American Oil prices for April will be the highest in five months. The Wheat suddenly went up according to Tuesday results despite the optimistic estimates by the USDA. According to the USDA forecasts, the world stocks before the harvest this year will increase by 5.7% for the first time since 2009/10. The EU raised its forecast for wheat production in its countries by 500 tons to 143.6 million tons for this year.

News

Is Bitcoin Price Recovery Real or Just a Temporary Bounce

Bitcoin dropped sharply through early 2026, falling to around...

Trading Gold (XAUUSD) Under the New Fed Chair

Kevin Warsh is taking over the Federal Reserve with a clear mission...

FedEx Sues Brooklyn Law Firm Over Fake Accident Claims

FedEx moves nearly everything Americans buy, from groceries to...

30-year Treasury yield has crossed 5%

The 30-year Treasury yield has crossed 5% , let’s see who pays...

Oil Price Analysis 2026 May

WTI crude futures fell below the $93 per barrel mark this morning,...

Why Oil Prices Could Crash to $60

Kevin Warsh is the frontrunner to lead the Federal Reserve, and...

Explore our

Trading Conditions

- Spreads from 0.0 pip

- 30,000+ Trading Instruments

- Stop Out Level - Only 10%

Ready to Trade?

Open AccountSee Also