- Analytics

- Market Overview

Stocks rally pauses - 22.12.2016

Dow fails to break above 20000 yet

US stock indices closed lower on Wednesday as Dow failed to break above 20000. The dollar pulled back with investors consolidating recent gains. The live dollar index data show the ICE US Dollar index, a measure of the dollar’s strength against a basket of six rival currencies, closed 0.25% lower at 103.026. The S&P 500 ended 0.1% lower settling at 2265.18 weighed by losses in health care stocks, with eight of its eleven main sectors finishing in the red. The Dow Jones industrial average ended 0.2% lower at 19941.96, yet again closing below the psychologically important level 20000 and retreating from the all-time high set the previous day. Losses in biotechnology shares pulled down the high tech index Nasdaq 0.2% to 5471.43.

The recent stock market rally paused as investors lost appetite for risky assets which was buoyed by Trump’s proclaimed support for expansionary policies such as tax cuts and big infrastructure projects. It is yet to be seen how they will be implemented after inauguration. In economic news, a housing report showed that sales of existing homes rose 0.7% in November constrained by low inventory and rising prices, but the pace of sales at a seasonally adjusted annual rate of 5.61 million, according to the National Association of Realtors, was the highest since 2007. Today at 14:30 CET third quarter final GDP, core Personal Consumption Expenditures, preliminary November Durable Goods Orders will be published in US. At the same time Initial Jobless Claims and Continuing Claims will be released, the outlook is positive for dollar. And at 16:00 CET November Personal Spending, Personal Income and Conference Board Leading Indicators will be released, the outlook is positive for dollar.

Italy’s parliament approves bank rescue loan

European stocks pull back from 2016 highs with falling bank shares dragging the market lower on Wednesday. The euro ended higher while the British Pound weakened against the dollar as data showed the £12.6 billion ($15.5 billion) the UK government borrowed in November compared with the year-earlier period was higher than expected. The Stoxx Europe 600 ended 0.5% lower. Germany’s DAX 30 outperformed as it edged up 3.9 points to 11468.64. France’s CAC 40 fell 0.3% and UK’s FTSE 100 index inched down less than 0.1% to 7041.42.

Spanish banks fell on prospect of repaying billions of euros to borrowers after the European Court of Justice decided that borrowers should be eligible for full reimbursements of excess interest payments on variable-rate mortgages. Banco Popular Espanol SA dropped 5.8%. Italian bank stocks inched higher after Italy’s parliament approved a government request for a rescue loan of up to 20 billion euros ($20.81 billion) to support the country’s ailing banking sector. Shares of Banca Monte dei Paschi di Siena sank 12.1% as the bank appears to be falling short of €5 billion in capital by the end of month or risk being wound down by European regulators. Shares in Deutsche Bank lost 0.4% and Societe Generale slipped 0.3% after Swiss Competition Commission said it had reached an “amicable settlement” with Royal Bank of Scotland, Barclays, Deutsche Bank and Societe Generale over their participation in the Euribor cartel. RBS and Barclays also settled investigations into cartels to manipulate Yen Libor, Swiss franc interest rate derivative pricing and the Swiss franc Libor benchmark rate. RBS shares rose 0.9% and Barclays ended up 0.5%. Today at 10:00 CET the European Central Bank will be publish the Economic Bulletin.

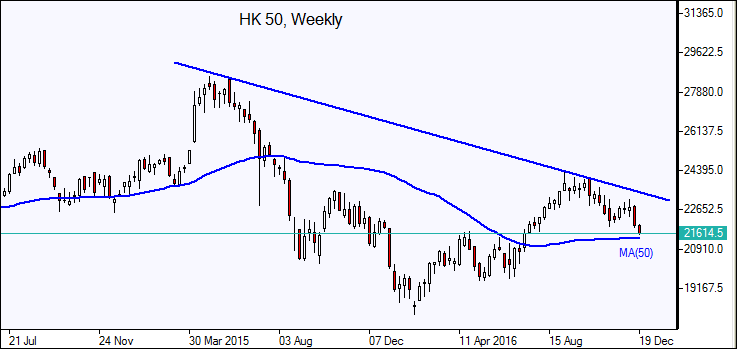

Asian stocks mixed ahead of holidays

Asian stocks are mixed today as investors are reluctant to make big bets in the run-up to the Christmas holidays. Nikkei fell 0.1% to 19427.67 despite a weaker yen against the dollar. Investors booked gains after the index hit one-year highs the previous day, pulling down financial stocks while exporter shares advanced. Chinese property stocks were under pressure after President Xi Jinping confirmed China will limit credit flowing into property speculation in 2017 and restrain property bubbles: the Shanghai Composite Index is up 0.1% and Hong Kong’s Hang Seng index is 0.8% lower. Australia’s All Ordinaries Index gained 0.5% while the Australian dollar edged higher against the dollar.

Oil prices pull back on surprise US inventory build

Oil futures prices are retreating today after a surprise report of the Energy Information Administration US crude stocks climbed by 2.3 million barrels instead of an expected decline of 2.5 million barrels. An additional negative for the oil market was Libya's National Oil Corporation announcement it hoped to add 270000 barrels per day (bpd) to national production after it confirmed on Tuesday that pipelines leading from the Sharara and El Feel fields had reopened. Libya recently doubled output to 600,000 bpd. February Brent crude closed 1.6% lower at $54.46 a barrel on Wednesday on London’s ICE Futures exchange.

- Get Certificate

Explore our

Trading Conditions

- Spreads from 0.0 pip

- 30,000+ Trading Instruments

- Instant Execution

Ready to Trade?

Open Account