- Analytics

- Market Overview

The Dollar Index made significant fluctuations on Friday, but, as a result, remained almost unchanged - 10.3.2014

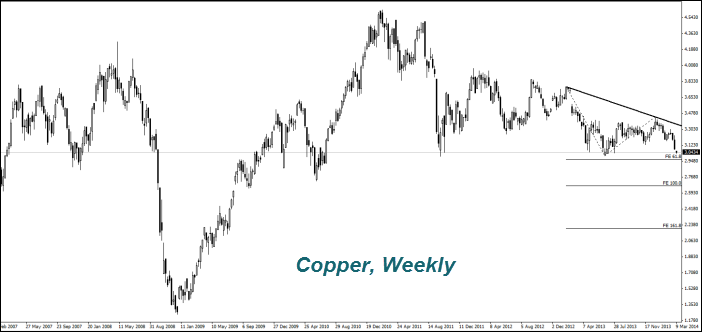

Note that there was a noticeable weakening of the Japanese Yen (rise on the chart) on Friday due to weak macroeconomic information. The GDP growth in the fourth quarter was worse than expected and amounted to 0.7% in annual terms. The current account deficit was also weaker than it had been expected. This is especially negative for export-oriented Japanese economy. However, the data from China have caused a change towards the Yen and it strengthened its position today (fall in the chart). Investors see the Yen as a safe heaven currency in the case of economic problems in China. This week macroeconomic data will be brought from Japan everyday, so the Yen can be quite volatile. Now market participants are focused on the results of the BOJ meeting, which will be announced on Tuesday. It is expected to continue easing the monetary policy aimed at weakening the exchange rate: emission 60-70 trillion Yen per year to redeem Japanese government bonds and the sales tax increase from 5% to 8% since April 1st. Because of the fall in Chinese exports, the Copper price in Shanghai on Friday fell by 5% to its lowest level in more than four years. Meanwhile, imports of Copper to China in January-February 2014 increased by 41.2% to 915 thousand tons compared to the previous year. Therefore, we believe that falling prices may be short-lived. China consumes 45% of world's Copper production. It is not excluded that the quotations were also affected by the first corporate default on the bonds in China in addition to weak exports. The solar energy equipment manufacturer, Solar Shaori did not pay any percentage on its debt securities. The Copper is actively used in the industry.

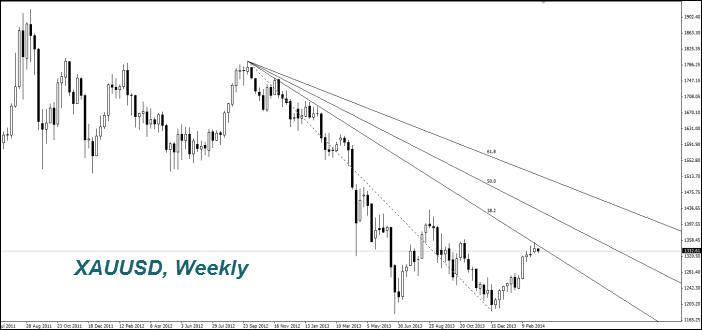

The Gold (XAUUSD) comes cheaper for the second consecutive day. Investors believe that the U.S. labor market data is acceptable for further economic growth. The political situation has been stabilized around Crimea partly on anticipation of a general referendum of its residents on March 16th. It will decide the future status of the peninsula. An additional factor of reducing the Gold price are the signs of a slowdown in Chinese economy. Meanwhile, according to the U.S. Commission on Commodity Futures Trading (CFTC), the number of net long positions on the Gold (net-long) last week increased by 3.8% to the highest level since December 2012, 118.2 thousand contracts. In this regard we can not exclude the resumption of growth in the Gold prices after the correction.

News

Inside Paramount’s $111 Billion Deal Pause

When Paramount Skydance announced it was putting its massive...

What the Oil Price Drop Really Means

Oil prices took a sharp drop on Sunday evening 5 % after the...

China-Us Supply Chain Competition

China added 10 more American companies to its entities list and...

Is Bitcoin Price Recovery Real or Just a Temporary Bounce

Bitcoin dropped sharply through early 2026, falling to around...

Trading Gold (XAUUSD) Under the New Fed Chair

Kevin Warsh is taking over the Federal Reserve with a clear mission...

FedEx Sues Brooklyn Law Firm Over Fake Accident Claims

FedEx moves nearly everything Americans buy, from groceries to...

Explore our

Trading Conditions

- Spreads from 0.0 pip

- 30,000+ Trading Instruments

- Stop Out Level - Only 10%

Ready to Trade?

Open AccountSee Also