- Analytics

- Market Overview

Global stock indexes fell on Wednesday - 15.5.2014

Global stock indexes fell on Wednesday. In our opinion, the main negative factor came from the United States. The PPI growth in April was higher than expected and it was the maximum for a year and a half (+0.6%). Its growth in March, was also quite significant (0.5%). Now, year by year PPI is 2.1%. Investors fear that the U.S. inflation may also increase to 2% per annum.

Recall that it will be announced today at 12.30 CET. The New York Empire Manufacturing for May is coming out simultaneously. Thereafter, we will see the industrial production index for April at 13-15 CET. The Philly manufacturing is coming out at 14-00 СЕТ. In our opinion, the forecast on the U.S. economic data is negative for the stock market. Nevertheless, futures on U.S. stock indices are rising this morning after European stocks. Note that the S&P 500 exceeded 1900 points on Tuesday for the first time and set a new historic peak.

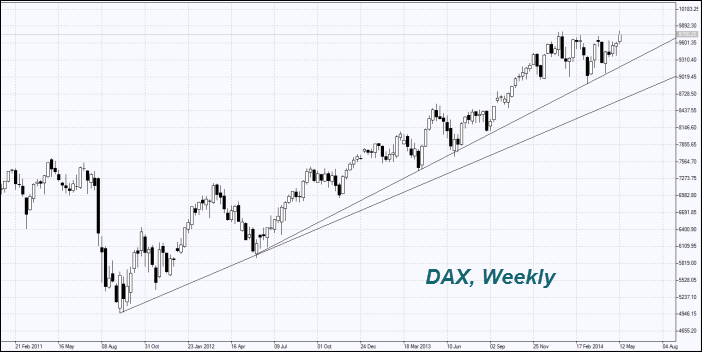

European stocks are growing this morning before the important macroeconomic information is released. German DAX set a new historic high due to the GDP growth in Germany by 0.8% in the first quarter. This is more than expected. At 9-00 CET, we will see the first quarter GDP announced and inflation in the EZ for April. The forecasts are positive for the stock market.

The Japanese Nikkei Index was closed with a slight disadvantage. In our opinion, the strong Yen increase in the sales tax from the first part of April may reduce corporate earnings. Investors even ignored the good GDP growth in the first quarter by 5.9% in annual terms. The data came out tonight. The additional negative outlook was from the Sony Company. It is going to suffer losses for the second consecutive year that caused a drop in the share price by 6.9%. Note that tomorrow at 4-30 CET, there will be the industrial production data in Japan released for March and there will be no other significant macroeconomic information expected for this week.

The Wheat prices tumbled to 3-week low, due to the favorable weather forecast in the Midwest over the next two weeks. The additional negative outlook came from China National Grain and Oils Information Centre (CNGOIC), according to which the total cereal production (wheat, maize and rice) in the season 2014/2015 is expected to increase by 1.7% to 552.14 million tons. Meanwhile, the import of the three crops into China will be reduced by 34.3% to 11.5 million tons. The Wheat crop can be at 122.6 million tons, 0.7% higher than in the previous season. Its imports, according to CNGOIC, reduced to 3 million tons from 7 million tons a season earlier.

The Corn significantly decreased due to the rumors that China could already start selling it from its state reserves next week, representing 70 million tons. The additional negative factor, as in the case of wheat, was the CNGOIC forecast. The corn production in the season 2014/2015 may increase by 2% and reach 222.1 million tons. While its imports are expected to decline to 3.5 million tons from 5.5 million tons last season.

The Oil (Oil, Brent) fell slightly after the announcement of the American Agency Energy Information Administration about its production increase in the United States by 78 thousand barrels per day (bpd) to 8.43 million bpd. This is due to the active development of Bakken shale in North Dakota and Eagle Ford in Texas. Meanwhile, another agency - the International Energy Agency (IEA) increased the global oil demand this year and lowered its forecast for production by non OPEC countries due to problems with Kashagan minefield in Kazakhstan, as well as the minefields in Colombia and South Sudan. According to the IEA, the OPEC must urgently increase the production to 30 million bpd. This issue will be discussed at the meeting in June. The OPEC has increased the production by 405 thousand bpd to 29.9 million bpd in April. However, it could not reduce quotes significantly as we can see. Note that according to the majority of European consumers the acceptable Brent Oil price is $102 per barrel.

News

China-Us Supply Chain Competition

China added 10 more American companies to its entities list and...

Is Bitcoin Price Recovery Real or Just a Temporary Bounce

Bitcoin dropped sharply through early 2026, falling to around...

Trading Gold (XAUUSD) Under the New Fed Chair

Kevin Warsh is taking over the Federal Reserve with a clear mission...

FedEx Sues Brooklyn Law Firm Over Fake Accident Claims

FedEx moves nearly everything Americans buy, from groceries to...

30-year Treasury yield has crossed 5%

The 30-year Treasury yield has crossed 5% , let’s see who pays...

Oil Price Analysis 2026 May

WTI crude futures fell below the $93 per barrel mark this morning,...

Explore our

Trading Conditions

- Spreads from 0.0 pip

- 30,000+ Trading Instruments

- Stop Out Level - Only 10%

Ready to Trade?

Open AccountSee Also